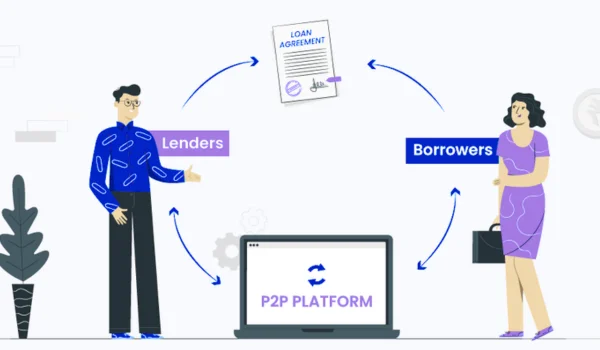

Borrowing money in the United States is no longer limited to banks and credit unions. Over the past decade, a new way of borrowing has become popular:

👉 Peer-to-Peer (P2P) lending

This system connects borrowers directly with individual investors through online platforms—cutting out traditional banks.

But is it safe? Is it cheaper? And should you use it?

In this complete guide, I’ll explain everything in simple English so you can clearly understand how P2P lending works in the U.S. and whether it’s right for you.

💡 What Is Peer-to-Peer Lending?

Peer-to-peer lending (also called social lending) is a method where:

👉 People (investors) lend money directly to other people (borrowers) through online platforms.

Instead of a bank giving you a loan, individual investors fund your loan.

📌 Simple Example

- You need: $10,000

- You apply on a P2P platform

- 100 investors contribute $100 each

- You receive the full amount

👉 You repay monthly with interest, and investors earn returns.

🏦 Popular Peer-to-Peer Lending Platforms in the US

Let’s look at the most trusted platforms.

- LendingClub

✔ Overview:

One of the oldest and most popular P2P platforms in the U.S.

✔ Loan Amount:

$1,000 – $40,000

✔ Best For:

- Personal loans

- Debt consolidation

✔ Features:

- Fixed interest rates

- Flexible repayment terms

- Prosper

✔ Overview:

Another leading P2P platform with millions of users.

✔ Loan Amount:

$2,000 – $50,000

✔ Best For:

- Medical expenses

- Home improvement

✔ Features:

- Quick approval

- Transparent fees

- Upstart

✔ Overview:

Uses AI to evaluate borrowers beyond just credit score.

✔ Best For:

- Low or limited credit history

✔ Features:

- Considers education and job history

- Faster approvals

- Funding Circle

✔ Overview:

Focused on small business loans.

✔ Loan Amount:

Up to $500,000

✔ Best For:

- Small business owners

⚙️ How Peer-to-Peer Lending Works (Step-by-Step)

📝 Step 1: Apply Online

You submit:

- Personal details

- Income information

- Credit history

📊 Step 2: Risk Assessment

The platform assigns you a risk grade based on:

- Credit score

- Income

- Debt level

💰 Step 3: Loan Listing

Your loan request is listed for investors to fund.

🤝 Step 4: Investors Fund Your Loan

Multiple investors contribute small amounts.

💵 Step 5: Receive Money

Once fully funded, money is transferred to your bank account.

📅 Step 6: Repayment

You repay monthly (principal + interest).

📊 P2P Lending vs Traditional Bank Loans

| Feature | P2P Lending | Bank Loan |

| Approval Speed | Fast | Slower |

| Credit Requirements | Flexible | Strict |

| Interest Rates | Moderate | Lower (if good credit) |

| Process | Online | In-person/online |

| Funding Source | Individual investors | Bank |

💰 Interest Rates in P2P Lending

Rates depend on your credit profile.

Typical Range:

- Good credit: 6%–10%

- Average credit: 10%–20%

- Poor credit: 20%+

👉 Still often cheaper than credit cards.

✅ Advantages of P2P Lending

✔ 1. Easier Approval

Even with average or low credit.

✔ 2. Fast Process

Approval in 1–3 days.

✔ 3. Flexible Use

Use money for:

- Debt consolidation

- Medical bills

- Travel

- Emergencies

✔ 4. Fixed Payments

Predictable monthly installments.

❌ Disadvantages of P2P Lending

❌ 1. Higher Rates for Low Credit

Can be expensive.

❌ 2. Origination Fees

Usually 1%–8% of loan amount.

❌ 3. Not Available in All States

Some restrictions apply.

❌ 4. Credit Impact

Late payments hurt your score.

💡 Who Should Use P2P Loans?

P2P lending is ideal for:

👉 People with:

- Fair or average credit

- Need quick approval

- Want to avoid banks

- Need unsecured loans

🚫 Who Should Avoid It?

Avoid P2P loans if:

- You have excellent credit (banks may offer better rates)

- You need very large loans

- You can’t handle monthly payments

🧠 Smart Tips Before Applying

✔ Compare Platforms

Check at least 2–3 options.

✔ Check APR (Not Just Interest)

Includes fees.

✔ Borrow Only What You Need

Avoid unnecessary debt.

✔ Read Terms Carefully

Understand repayment schedule.

⚠️ Common Mistakes to Avoid

❌ 1. Ignoring Fees

Origination fees can increase cost.

❌ 2. Missing Payments

Damages your credit score.

❌ 3. Over-Borrowing

Leads to debt problems.

❌ 4. Not Comparing Options

You may miss better deals.

💰 Real-Life Example (USA Scenario)

Let’s say you live in Chicago and have:

- Credit card debt: $8,000

- Interest rate: 22%

You apply on:

- LendingClub

You get:

- Loan: $8,000

- Interest rate: 12%

👉 Result:

- Lower monthly payment

- Save thousands in interest

📈 Is P2P Lending Safe?

Yes, if you use trusted platforms.

These platforms:

- Follow U.S. regulations

- Use secure systems

- Report to credit bureaus

👉 Always avoid unknown or unverified apps.

🔄 Future of P2P Lending in the US

P2P lending is growing because:

- People prefer online services

- Faster approvals

- More flexible lending

👉 It’s becoming a strong alternative to traditional banks.

🏁 Final Thoughts

Peer-to-peer lending in the U.S. offers a modern, flexible way to borrow money.

It’s especially helpful if:

- You don’t want bank hassle

- You need quick funds

- Your credit isn’t perfect

📌 Simple Rule to Remember

👉 “P2P lending connects people, not just money.”

If used wisely, it can help you:

✔ Save money

✔ Pay off debt faster

✔ Handle emergencies