Let’s start with a real situation many American families face.

Robert, a 68-year-old retiree in Miami, Florida, passed away unexpectedly. His family was already struggling with rising living costs. Within days, they were hit with:

- Funeral expenses: $9,000

- Medical bills: $4,500

- Credit card debt: $6,000

Total burden: nearly $20,000

His children had to take loans just to cover these costs.

This is the reality in the US. Even after retirement, financial responsibilities don’t disappear. And without proper planning, your loved ones may face serious financial stress.

That’s why life insurance for seniors is so important.

The good news? There are low-cost life insurance options designed specifically for seniors—even if you’re on a fixed income.

In this guide, I’ll explain everything in simple terms so you can choose the right plan confidently.

What Is Life Insurance for Seniors?

Life insurance for seniors is a policy designed for people typically aged 50 to 85, providing a payout (death benefit) to beneficiaries after the policyholder passes away.

Simple idea:

👉 You pay monthly premiums → your family receives a lump sum after your death.

Why Seniors Still Need Life Insurance

Many people think life insurance is only for young families—but that’s not true.

Here’s why seniors need it:

- Funeral and Burial Costs

Average funeral cost in the US:

👉 $7,000 to $12,000

- Medical Bills

Even with Medicare, out-of-pocket expenses can be high.

- Debt Protection

- Credit cards

- Personal loans

- Mortgage (in some cases)

- Support for Family

Some seniors want to leave money for:

- Spouse

- Children

- Grandchildren

- Estate Planning

Helps cover taxes and legal expenses.

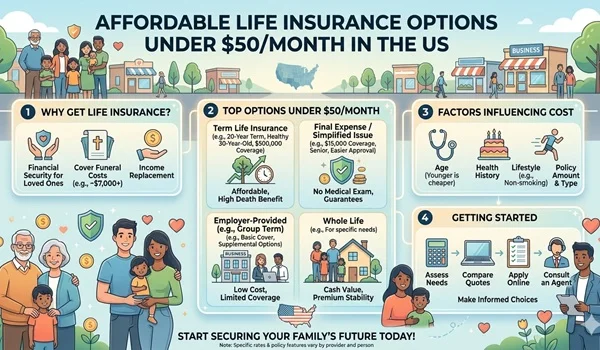

Types of Low-Cost Life Insurance for Seniors

Let’s break this down simply.

- Term Life Insurance (For Seniors)

- Coverage for a specific period (10–20 years)

- Lower cost compared to permanent plans

Example:

In Dallas, Texas:

- Age 60

- $100,000 coverage

👉 Around $80–$150/month

Best for:

✔ Healthy seniors

✔ Temporary coverage needs

- Whole Life Insurance (Permanent)

- Lifetime coverage

- Builds cash value

- Higher cost

Best for:

✔ Long-term protection

✔ Estate planning

- Final Expense Insurance (Most Popular)

Also called burial insurance.

- Small coverage ($5,000–$25,000)

- Easy approval

- No medical exam (in many cases)

Example:

In Phoenix, Arizona:

- Age 65

- $15,000 coverage

👉 $50–$120/month

Best for:

✔ Covering funeral costs

✔ Seniors with health issues

- Guaranteed Issue Life Insurance

- No medical questions

- Approval guaranteed

- Higher premiums

Catch:

- Waiting period (2–3 years for full benefits)

Comparison Table: Best Options for Seniors

| Feature | Term Life | Whole Life | Final Expense | Guaranteed Issue |

| Cost | Low | High | Moderate | Higher |

| Coverage Amount | High | Medium–High | Low | Low |

| Medical Exam | Usually required | Sometimes | Often not required | Not required |

| Approval Speed | Medium | Medium | Fast | Very fast |

| Best For | Healthy seniors | Long-term needs | Funeral costs | Health issues |

👉 Simple takeaway:

- Healthy seniors → Term life

- Most seniors → Final expense plans

How Much Does Life Insurance Cost for Seniors?

Costs depend on:

- Age

- Health

- Coverage amount

- Type of policy

Average Monthly Costs:

- Age 60: $50–$150

- Age 70: $80–$250

- Age 80: $150–$400

Example:

In Chicago, Illinois:

- Age 70

- $20,000 final expense plan

👉 Around $90/month

How to Choose the Right Plan (Step-by-Step)

Step 1: Decide Coverage Amount

Ask:

👉 How much money will my family need?

Example:

- Funeral: $10,000

- Debt: $5,000

👉 Total: $15,000 coverage needed

Step 2: Choose the Right Type

- Small needs → Final expense

- Larger needs → Term or whole life

Step 3: Check Your Health

- Healthy → More options, lower cost

- Health issues → Guaranteed or simplified plans

Step 4: Compare Multiple Quotes

Never buy the first policy.

Step 5: Read Policy Details Carefully

Check:

- Waiting periods

- Exclusions

- Premium increases

Smart Tips to Save Money

- Buy Earlier

Premiums increase with age—don’t delay.

- Choose Only What You Need

Don’t overbuy coverage.

- Consider Simplified Plans

No-exam plans can save time and hassle.

- Pay Annually (If Possible)

Some insurers offer discounts.

- Work With a Trusted Agent

They can find better deals.

Common Mistakes Seniors Should Avoid

Mistake 1: Waiting Too Long

Insurance becomes expensive after age 70–75.

Mistake 2: Buying Too Much Coverage

You don’t need a $500,000 policy if your goal is funeral costs.

Mistake 3: Ignoring Waiting Periods

Some policies don’t pay full benefits immediately.

Mistake 4: Not Telling Family About Policy

Your family should know how to claim it.

Mistake 5: Choosing Based Only on Price

Cheap plans may have limited benefits.

Real-Life Scenario

Let’s say:

You’re 72 years old in Los Angeles, California

You want to avoid burdening your family.

Option A:

- $10,000 final expense plan

- $75/month

Option B:

- No insurance

👉 If something happens:

- Option A → Family is protected

- Option B → Family pays out-of-pocket

Strategies for Seniors

Strategy 1: Focus on Final Expense Plans

Simple, affordable, and effective.

Strategy 2: Combine Savings + Insurance

Use insurance to cover gaps.

Strategy 3: Lock in Fixed Premiums

Avoid policies where costs increase over time.

Strategy 4: Review Your Needs Regularly

Your financial situation may change.

FAQs

- Can seniors get life insurance after 70?

Yes, many companies offer policies up to age 80 or even 85.

- What is the cheapest life insurance for seniors?

Final expense insurance is usually the most affordable option.

- Do I need a medical exam?

Not always—many plans offer no-exam options.

- What happens if I miss a payment?

Your policy may lapse, so set up auto-pay if possible

- Is life insurance worth it after retirement?

Yes—especially to cover funeral costs and protect your family from debt

Final Conclusion: What Should You Do Next?

Life insurance for seniors is not about building wealth—it’s about protecting your family from financial stress.

Even a small, affordable plan can make a big difference.

Your action plan:

- Calculate your final expenses (funeral + debts)

- Choose a suitable plan (final expense is best for most seniors)

- Compare at least 2–3 insurance providers

- Check for waiting periods and exclusions

- Buy a policy that fits your budget comfortably

👉 Simple rule:

“Don’t leave your family with bills—leave them with support.”

Take action today. Even a $50–$100 monthly plan can save your loved ones from thousands of dollars in unexpected expenses.